Table of Content

You can still get a good deal, historically speaking — especially if you’re a borrower with strong credit. Of course, rate volatility could increase due to the uncertainty of a recession or the repercussions of global events impacting the economy. This followed 248 basis points (2.48%) of growth in the year’s first half. Rates varied from one week to the next as the Fed wrestled with inflation. Mortgage rates experienced the largest weekly jump since 1987, surging 55 basis points (0.55%) the day after the Federal Reserve’s June hike.

Overall household wealth — which includes home values, stock portfolios and bank accounts minus mortgages and credit-card debt — spiked 80 percent over the last decade. What all of this means is that, essentially, the Fed is trying to maintain a relatively low interest rate environment…which should be good for mortgage rates in general. The national median sale price of an existing home is expected to grow to $270,400, an increase of 4.3 percent from 2019.

Mortgage rates are expected to remain historically high into 2023, but you can lower your interest rate today

A positive value indicates that GDP exceeds potential GDP; a negative value indicates that GDP falls short of potential GDP. By 2028, real GDP reaches its long-run level relative to potential GDP and grows at the same rate as potential GDP thereafter. The market for immuno-oncology drugs and therapies is expected to grow at a 15% CAGR, from $60 billion in 2021 to $194 billion by 2028. Higher rates mean more pain for the economy and corporate earnings and spur investors to move money from stocks to less risky bonds. Federal Reserve Board Chairman Jerome Powell speaks during a news conference after the Federal Reserve announced that it would raise interest rates by a 0.5 percentage point to 4.5.

Real GDP recovers rapidly over the next several quarters in CBO’s projections, rising from more than 6 percent below its potential at the end of 2020 to less than 4 percent below its potential at the end of 2021. The growth of real GDP then slows, and output remains far below its potential for several more years. The unemployment rate remains above its prepandemic level through the end of the projection period. The unemployment rate is projected to peak at over 14 percent in the third quarter of this year and then to fall quickly as output increases in the second half of 2020 and throughout 2021. Interest rates are rising, inflation is expected to hit eight per cent by the end of the year. Such developments bolster the economy but could well fuel more inflation.

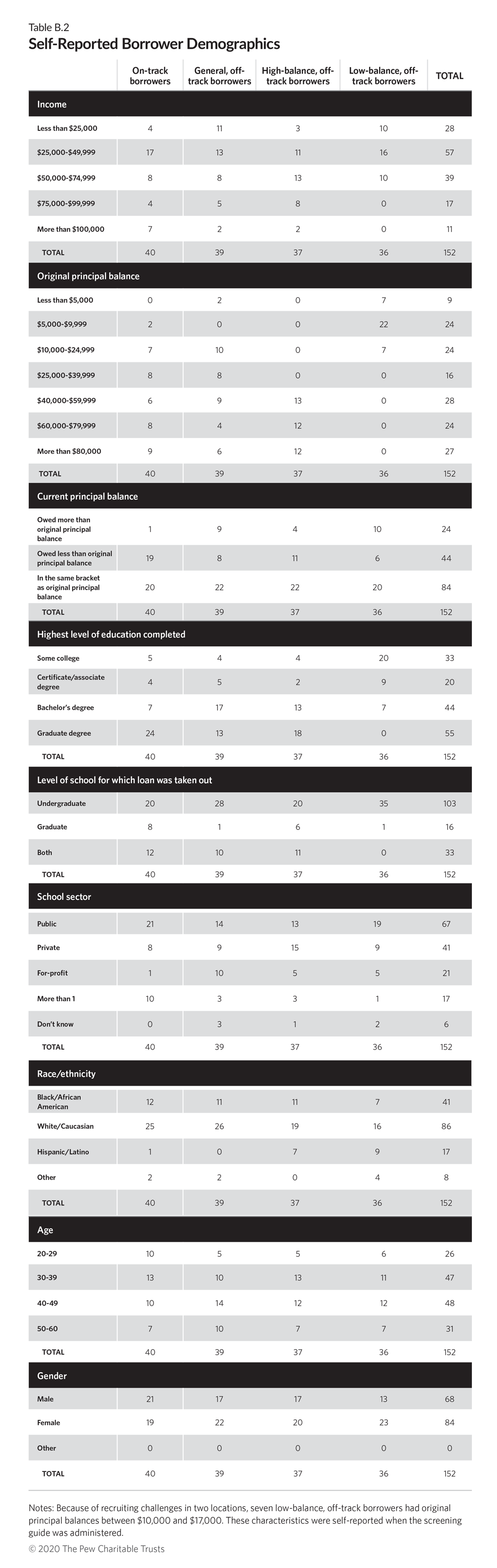

Current mortgage interest rates chart

Real values are nominal values that have been adjusted to remove the effects of changes in prices. It is similar to the May forecast for those two years, except that the projection of growth in the second half of 2020 has been revised downward. Meanwhile, the S&P 500 index has tumbled about 4% since the Fed announcement, giving back much of the 7.5% gain over the prior six weeks, sparked largely by the encouraging inflation reports and hopes for a less aggressive Fed. Consumer prices rose 7.1% annually in November, down from 8.2% in September and a 40-year high of 9.1% in June, according to the Consumer Price Index. Fed Chair Jerome Powell said the Fed has a “ways to go” before it takes a breather and holds rates steady. Savers might think they should cheer the news that rates will climb in 2022, but all signs point to a likelihood that offerings won’t be that much more attractive.

First-time buyers will continue to struggle with affordability, even with mortgage rates in an approachable range, as entry-level inventory is expected to remain constrained. The broad price moderation will continue to offer opportunities in mid-sized markets in the Midwest and South. Following the Federal Reserve’s monetary accommodation, inflation expectations remain modest and well-anchored, translating into a 2.0 percent year-over-year increase in 2020. While short term rates remain low, economic moderation is likely to impact bond markets, leading to mortgage rates moving mostly sideways in 2020. Rates for 30-year fixed mortgages are projected to average 3.85 percent during the next year.

Should you wait for lower rates?

After 2022, 10-year Treasury note interest rates are expected to rise steadily to 2.9 percent in the fourth quarter of 2023 and 3.1 percent in 2024. Even with today's exceptionally low mortgage rates, there's actually an unprecedented large gap between mortgage interest rates and the 10-Year Treasury Bonds — even though these normally move in lockstep. If mortgage rates followed past trends and this yields gap was narrowed, mortgage rates would actually be even lower than they are now. Sellers in 2020 will contend with flattening price growth and slowing activity, requiring more patience and a thoughtful approach to pricing. Sellers of homes priced for entry-level buyers can expect the market to remain competitive and prices to stay firm. At the upper end of the price range, however, properties will take longer to sell, and incentives will be needed to close deals.

Towards the midpoint of the year, however, the central bank’s policy shifted, in response to global changes. While the US economy continued showing signs of growth, major economies around the world slowed. In response to the slowdown, central banks around the world engaged in accommodative monetary responses, resorting to cutting rates and purchasing assets, in an effort to boost output. Along with the Bank of Japan, several central banks in Europe took interest rates into negative territory, attempting to spur investment and liquidity.

And so they feel they must raise interest rates higher than planned to make it more expensive for employers to borrow money to hire and invest, damping job growth and wage increases. In other words, the Fed is slowing the pace of its flurry of rate increases this year, which are intended to curtail high inflation. That will better allow the central bank to assess the effects of the aggressive moves, including whether they're about to tip the U.S. into a recession next year as most economists predict. Mortgage rates are currently trending down, but could begin to increase once again.

Interest rates decreased for the fifth straight week and reached their lowest point since September. However, the borrower would recoup the upfront cost over time thanks to the savings earned by a lower interest rate. However, record-low rates were largely dependent on accommodating, Covid-era policies from the Federal Reserve. And the more U.S. and world economies recover from their Covid slump, the higher interest rates are likely to go. Aaron Block, the co-founder of MetaProp—a venture capital fund focusing solely on real estate technology—says to keep an eye on the Airbnb and WeWork brands specifically in this regard.

The baseline forecast is being published now, rather than later with the budget projections, to provide the Congress with CBO’s current assessment of the economic outlook in a rapidly evolving environment. This economic forecast updates the interim forecast that CBO published in May, which focused on 2020 and 2021. This economic forecast provides CBO’s first complete set of economic projections through 2030 since January and incorporates information available as of June 26. This report presents the baseline economic forecast that the Congressional Budget Office is using as the basis for updating its budget projections for 2020 to 2030.

But you can shop for mortgage rates in under a day if you put your mind to it. And shaving just a few basis points off your rate can save you thousands. Your mortgage rate doesn’t have to be a long-term commitment, even with a fixed 30-year home loan. The pace slowed in the second quarter, then interest rates shot up again after the Fed’s 0.75% federal funds rate hikes in June, July, September, and November. The 30-year fixed-rate mortgage averaged 6.58% near the end of November, according to Freddie Mac. Only one of the six major housing authorities we looked at projects the fourth quarter average to finish below that.

For more details, read Bankrate’s home equity interest rate forecast. Our goal is to give you the best advice to help you make smart personal finance decisions. We follow strict guidelines to ensure that our editorial content is not influenced by advertisers. Our editorial team receives no direct compensation from advertisers, and our content is thoroughly fact-checked to ensure accuracy. So, whether you’re reading an article or a review, you can trust that you’re getting credible and dependable information.

Interestingly, that’s not the case….the Fed doesn’t make mortgage rates, they are driven by the bond market market on Wall Street. That will provide information about whether unemployment is continuing to increase following a flurry of layoffs in November and if job growth meaningfully slows. If so, that would be welcome news for mortgage rates to come down slightly as the Fed may become more cautious of a faltering labor market. The Fed is likely to keep hiking interest rates, which could lead to further mortgage rate increases. On the other hand, if the Fed’s actions lead to a recession, that could actually tug mortgage interest rates down.

No comments:

Post a Comment